03 · Return levels and return periods

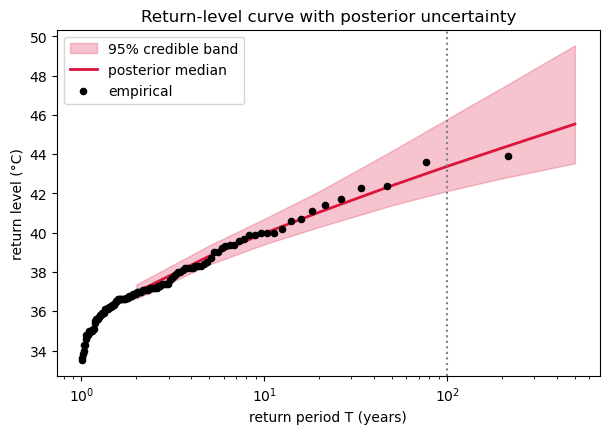

Engineers and planners rarely want directly — they want the return level : the value exceeded on average once every years. It is just a high quantile of the GEV,

xtremax gives this two ways: the distribution method .return_level(T) and the

pure primitive gev_return_level(T, loc, scale, shape). Because we have a

posterior over the parameters, we get a posterior over the whole return-level

curve — i.e. honest uncertainty bands.

import sys

import pathlib

try:

import spatial_extremes # noqa: F401 installed editable in the project venv

except ModuleNotFoundError:

_here = pathlib.Path.cwd().resolve()

_roots = (_here, *_here.parents)

_cands = [r / "src" for r in _roots]

_cands += [r / "projects" / "spatial_extremes" / "src" for r in _roots]

_src = next((c for c in _cands if (c / "spatial_extremes").exists()), None)

if _src is None:

raise RuntimeError("cannot locate spatial_extremes/src") from None

sys.path.insert(0, str(_src))import jax

jax.config.update("jax_enable_x64", True)import numpy as np

import jax

import jax.numpy as jnp

import jax.random as jr

import matplotlib.pyplot as plt

import numpyro

import numpyro.distributions as ndist

from numpyro.infer import MCMC, NUTS

from numpyro.infer.initialization import init_to_median

from xtremax import GeneralizedExtremeValueDistribution as GEV

from xtremax import gev_return_level

from spatial_extremes import data

maxima, stations, years, is_real = data.load_annual_maxima(min_years=20)

order = np.isfinite(maxima).sum(1) + np.nan_to_num(np.nanmean(maxima, 1)) / 1e3

sidx = int(np.argmax(order))

m_ = np.isfinite(maxima[sidx])

y = jnp.asarray(maxima[sidx][m_])

y_mean, y_std = float(jnp.mean(y)), float(jnp.std(y)) # constants, not tracers

def gev_model(obs):

mu = numpyro.sample("mu", ndist.Normal(y_mean, 5.0))

sigma = numpyro.sample("sigma", ndist.HalfNormal(y_std))

xi = numpyro.sample("xi", ndist.Normal(0.0, 0.25))

numpyro.sample("obs", GEV(loc=mu, scale=sigma, concentration=xi), obs=obs)

mcmc = MCMC(NUTS(gev_model, target_accept_prob=0.95, init_strategy=init_to_median),

num_warmup=800, num_samples=800, num_chains=1, progress_bar=False)

mcmc.run(jr.PRNGKey(0), y)

post = mcmc.get_samples()

print("source:", "REAL" if is_real else "SYNTHETIC", "| station", sidx)source: REAL | station 12

periods = jnp.array([2., 5., 10., 20., 50., 100., 200., 500.])

# posterior return-level curve: vmap over posterior draws

def rl(mu, sigma, xi):

return GEV(loc=mu, scale=sigma, concentration=xi).return_level(periods)

rls = jax.vmap(rl)(post["mu"], post["sigma"], post["xi"]) # (n_draws, n_periods)

med = np.median(rls, 0)

lo, hi = np.quantile(rls, 0.025, 0), np.quantile(rls, 0.975, 0)

# sanity check: the pure primitive agrees with the distribution method

prim = gev_return_level(100., float(np.median(post["mu"])),

float(np.median(post["sigma"])), float(np.median(post["xi"])))

print(f"100-yr return level (median): {med[5]:.1f} °C "

f"(primitive check: {float(prim):.1f} °C)")100-yr return level (median): 43.4 °C (primitive check: 43.4 °C)

Empirical return levels (Gringorten plotting positions) let us eyeball the fit:

ys = np.sort(np.asarray(y))

n = ys.size

emp_p = (np.arange(1, n + 1) - 0.44) / (n + 0.12) # Gringorten

emp_T = 1.0 / (1.0 - emp_p)

fig, ax = plt.subplots(figsize=(7, 4.5))

ax.fill_between(np.asarray(periods), lo, hi, alpha=0.25, color="crimson",

label="95% credible band")

ax.plot(np.asarray(periods), med, color="crimson", lw=2, label="posterior median")

ax.scatter(emp_T, ys, color="k", s=20, zorder=5, label="empirical")

ax.axvline(100, ls=":", color="0.5")

ax.set_xscale("log")

ax.set_xlabel("return period T (years)")

ax.set_ylabel("return level (°C)")

ax.set_title("Return-level curve with posterior uncertainty")

ax.legend()

plt.show()

Next: do this for every station and map the parameters — exposing why we need to pool information across space.